Indian Pharmaceutical Industry: Impact of the Iran–USA–Israel Geopolitical Crisis – 2026

DEEP STUDY REPORT

Indian Pharmaceutical Industry:

Impact of the Iran–USA–Israel Geopolitical Crisis

Supply Chains • Exports • API Costs • Energy Risks • Strategic Opportunities

Executive Summary

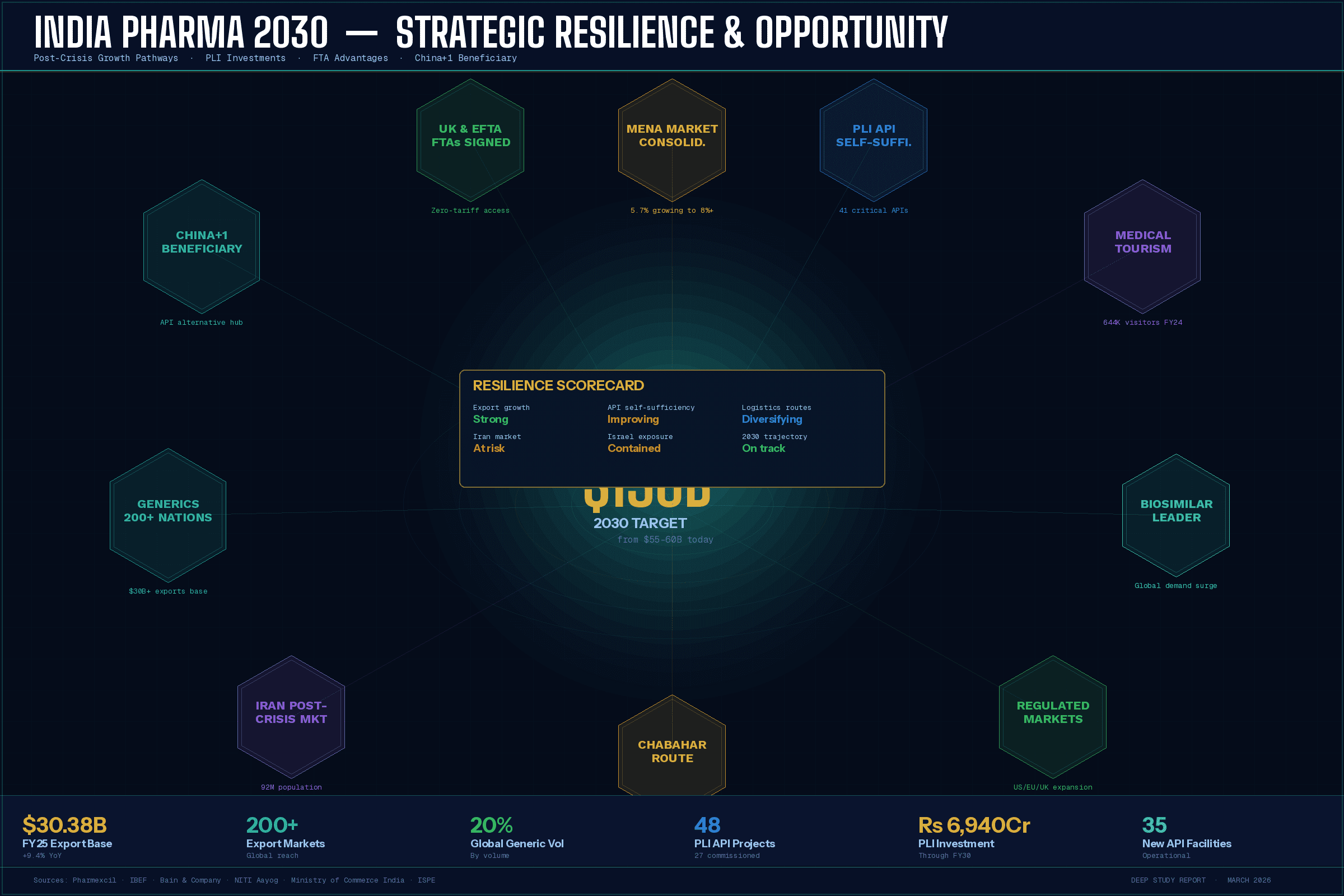

| India, the self-styled ‘Pharmacy of the World’, faces compounding geopolitical pressures from the Iran-USA-Israel crisis. While the sector has demonstrated structural resilience — growing exports to $30.38 billion in FY25 — escalating regional instability poses multi-dimensional threats across energy costs, logistics, export markets, corporate investments, and strategic partnerships. |

The Indian pharmaceutical industry, accounting for approximately 20% of global generic drug supply by volume, stands at a critical juncture. The widening conflict involving Iran, the United States, and Israel — encompassing military strikes, sanctions regimes, maritime chokepoints, and airspace closures — has created an interlocking web of vulnerabilities for Indian pharma’s global operations.

This report synthesises findings from industry surveys, trade data, expert analyses, and policy developments between October 2023 and March 2026 to deliver a comprehensive assessment of the crisis impact.

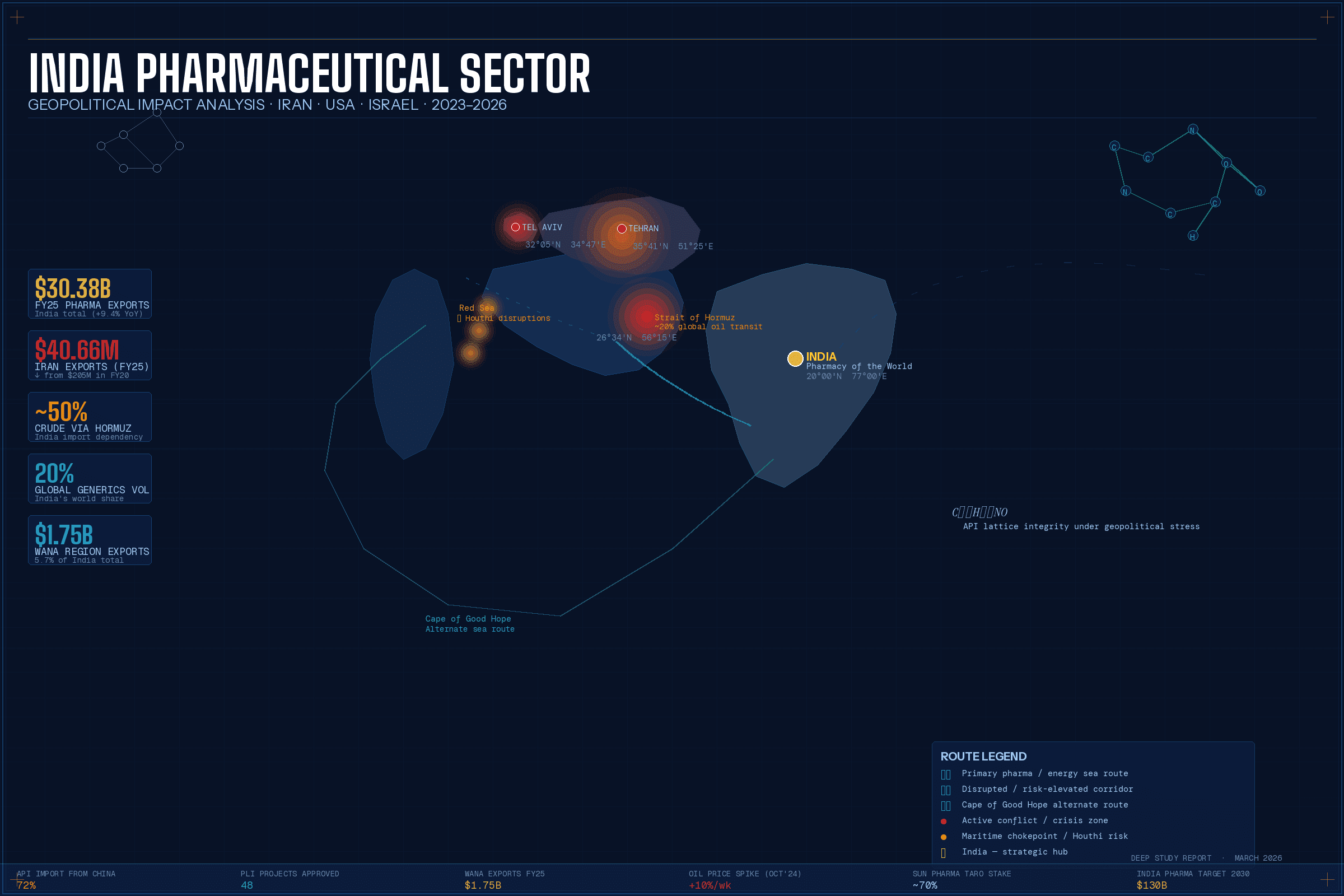

| $30.38B India Total Pharma Exports (FY25) +9.4% YoY | $1.75B WANA Region Exports 5.7% of total | $205M Iran Pharma Exports (FY20) FY25: Only $40.66M | ~50% Crude Oil via Hormuz of India’s total imports |

1. Background: India’s Pharma Industry at a Glance

India occupies a uniquely strategic position in the global pharmaceutical landscape. Known as the ‘Pharmacy of the World’, India is the third-largest producer of drugs by volume globally, holds the highest number of US FDA-approved manufacturing plants outside the United States, and serves as the primary source of affordable generic medicines for over 200 countries.

1.1 Key Industry Metrics (FY25)

| Parameter | Value / Status | Notes |

| Total Industry Valuation | ~$55–60 Billion | As of 2025 |

| Total Pharma Exports | $30.38 Billion | FY25 (+9.4% over FY24) |

| Global Generic Market Share | ~20% | By volume |

| US FDA Plants Outside USA | Highest Globally | Quality benchmark |

| Export Markets | 200+ Countries | Including US, UK, EU, Africa |

| Projected Value (2030) | $130 Billion | Government target |

| Direct & Indirect Employment | 2.7 Million | Livelihoods supported |

The top five export destinations in FY25 were the USA (34.61%), UK (3.01%), Brazil (2.56%), France, and South Africa. Formulations and biologics constitute 79.26% of exports, with bulk drugs and intermediates at 16.08%. The industry’s deep integration into global healthcare supply chains makes it acutely sensitive to geopolitical shocks.

1.2 The Iran–USA–Israel Crisis: A Timeline

The crisis has unfolded in cascading phases since October 2023:

- October 2023: Israel–Hamas war begins in Gaza; regional escalation concerns emerge immediately for pharma supply chains.

- April 2024: Iran launches unprecedented drone and missile attack on Israel; Indian pharma industry placed on high alert.

- October 2024: Retaliatory Israeli strikes on Iranian infrastructure; Brent crude surges over 10% in a week.

- June 2025: US and Israeli forces conduct military strikes on Iranian nuclear and military facilities; oil prices spike sharply.

- June–July 2025: Ceasefire brokered; oil prices moderate from peaks but uncertainty persists.

- March 2026 (current): New US-Iran tensions re-emerge; fresh airspace closures and shipping disruptions affecting India directly.

2. Impact on India–Iran Pharmaceutical Trade

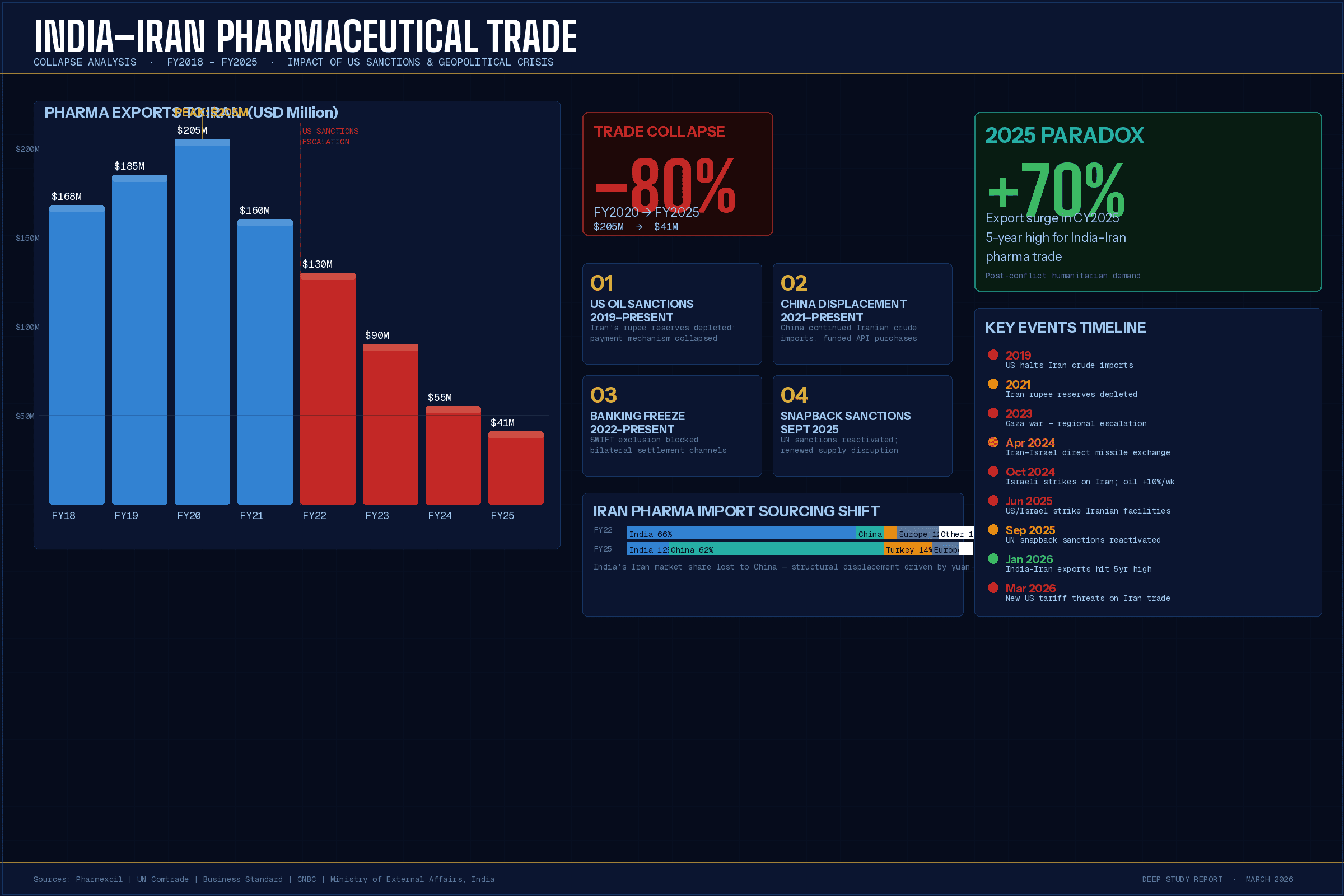

2.1 The Sharp Decline: From $205M to $40M

India’s pharmaceutical trade with Iran illustrates how geopolitical events can devastate bilateral commercial ties. Iran, with a population of nearly 92 million — ranking 17th globally — should theoretically represent a major pharmaceutical market for India. However, the reality has been a dramatic and sustained collapse in trade.

| $205M India Pharma Exports to Iran (FY20) Pre-sanctions peak | $40.66M India Pharma Exports to Iran (FY25) Crisis-era trough | -80% Decline Over 5 years | 0.13% Iran’s Share of India Exports (FY25) Far below potential |

The root cause is the cascade of US sanctions on Iran. When India halted crude oil imports from Iran in 2019 following US sanctions imposed over Iran’s nuclear programme, the rupee-denominated trade mechanism that underpinned pharmaceutical exports collapsed. Iran’s rupee reserves — accumulated through oil payments — were depleted, leaving no mechanism to pay Indian suppliers.

| Key Finding: Pharmaceutical exports declined 71.25% in the first five months of 2023 alone, and 31.29% in FY23 overall, according to Pharmexcil data. The trade that once sustained livelihoods for scores of Indian bulk drug manufacturers has been almost entirely displaced by Chinese competitors, who continued purchasing Iranian crude even post-sanctions and accumulated yuan reserves to fund bulk drug purchases. |

2.2 China’s Strategic Displacement of India

Perhaps the most strategically consequential long-term impact of the sanctions regime has been the structural shift in Iran’s pharmaceutical import sourcing. While India stopped oil imports from Iran in compliance with US pressure, China continued buying discounted Iranian crude, accumulating yuan reserves that Tehran could deploy for pharmaceutical imports.

UN Comtrade data shows that in 2021, Iran’s imports of formulations from China grew 91.1%, from the Netherlands 62.2%, and from Turkey 205%. Indian pharmaceutical exports — primarily bulk drugs and intermediates comprising about 65% of the export basket — suffered permanent market share erosion. Reversing this trend will require not just political will but structural trade finance innovation.

2.3 The Snapback Sanctions and Renewed Shortages (2025)

The reactivation of UN snapback sanctions on Iran in September 2025 further deepened the crisis. Iranian pharmaceutical industry officials warned of inevitable production disruptions and severe drug shortages, noting that while 99% of domestic medicines are produced locally, a significant share of active pharmaceutical ingredients (APIs) and key stabilising compounds still come from India, China, and Europe.

Iran’s pharmaceutical industry, overseen by the IFDA, includes 347 enterprises producing approximately $1.8 billion worth of medicines annually. Despite high domestic self-sufficiency, critical API dependencies on India create a vulnerability that US sanctions exploit indirectly — not by targeting pharmaceutical trade (which has humanitarian exemptions), but by making payment mechanisms dysfunctional.

2.4 The Paradox: Record Exports Amid Crisis (2025)

Paradoxically, data from January 2026 showed Indian pharmaceutical exports to Iran hitting a five-year high in calendar year 2025, surging 70% compared to 2024. This reflects a period of humanitarian exemption utilisation, partial easing of payment restrictions, and urgent demand during the post-conflict health emergency in Iran. However, Trump administration threats of an additional 25% tariff on countries trading with Iran in early 2026 renewed uncertainty for Indian exporters.

3. Impact on India–Israel Pharmaceutical Relations

3.1 Deeper Ties: Investment and Talent

India’s relationship with Israel’s pharmaceutical sector is characterised by investment and talent flows rather than commodity trade. India’s pharmaceutical exports to Israel were $0.14% of total exports in FY25 — a relatively modest figure given Israel’s population of 10.1 million. However, the strategic depth of the relationship lies elsewhere.

Israeli pharmaceutical companies, most notably Teva Pharma (established in 1901 as SLE Limited), have maintained a substantial presence in India. Teva’s Indian manufacturing base serves its global generics portfolio. Major Indian companies including Sun Pharma, Dr Reddy’s, and Cipla have actively recruited senior talent from Israel’s pharmaceutical sector.

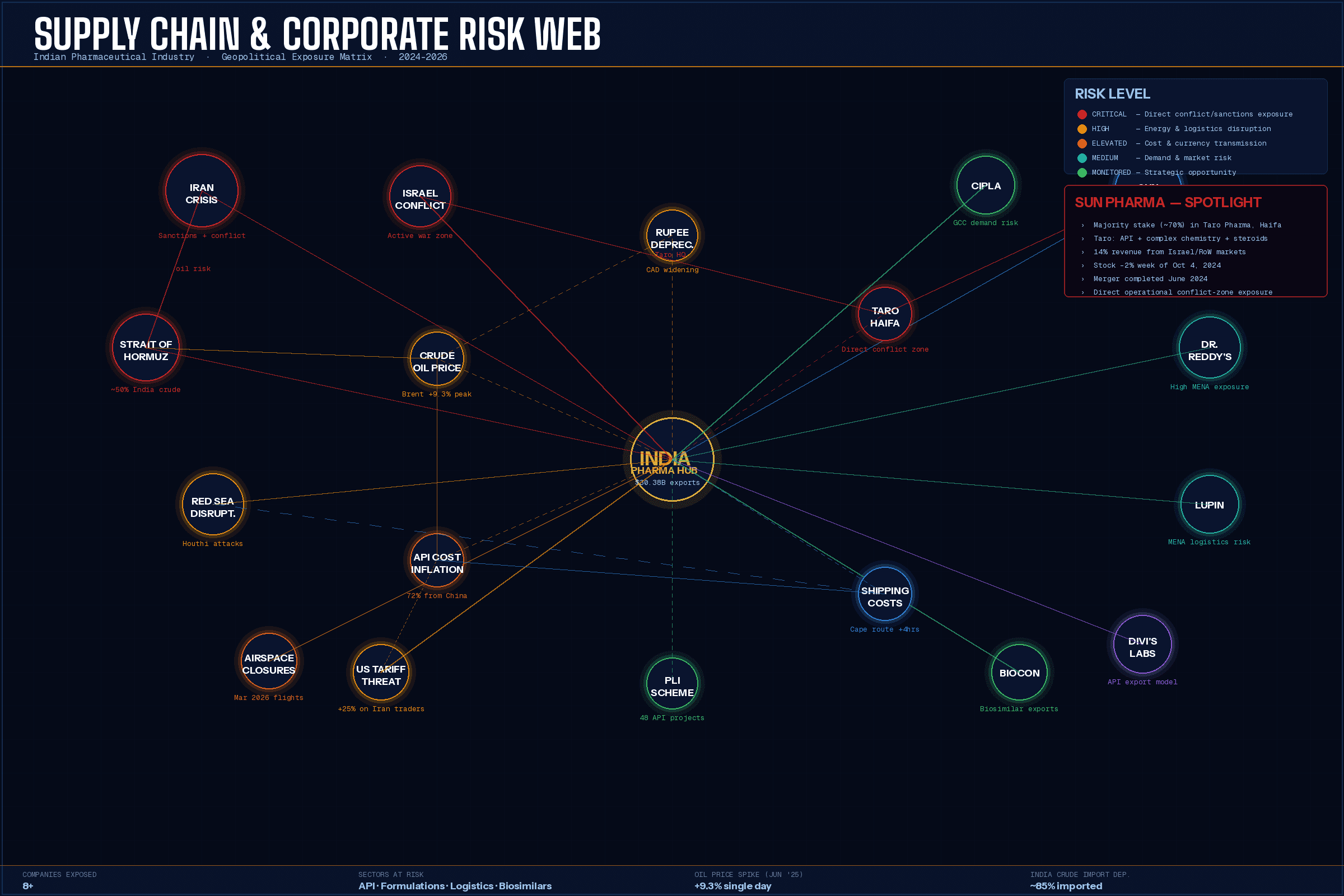

3.2 Sun Pharma and Taro: Direct Conflict Zone Exposure

| Sun Pharmaceutical Industries holds a majority stake (approximately 70%) in Taro Pharmaceutical Industries, headquartered in Haifa, Israel. Taro — whose name derives from the Hebrew word for ‘pharmaceutical industry’ — was incorporated in 1959 and specialises in generic drugs, complex chemistry, and steroids. Sun Pharma, after 17 years of acquisition proceedings, completed the full Taro merger in June 2024. |

The conflict has had direct operational implications for Sun Pharma through Taro. Taro’s manufacturing sites in Israel produce APIs including complex chemistry and steroid formulations. Conflict-related disruptions to Israeli infrastructure, logistics, and labour availability have affected Taro’s production continuity. Sun Pharma’s shares declined approximately 2% in the week ended October 4, 2024 — against a BSE Sensex decline of 4.5% — reflecting direct investor concern about conflict-zone exposure.

Sun Pharma generates approximately 14% of its total revenue from ‘rest of world’ markets that include Israel, Western Europe, Canada, Japan, Australia, and New Zealand. Any sustained disruption at Taro’s Israeli operations affects global supply of specialised generics.

3.3 Adani Ports and Strategic Infrastructure

Complementing the pharma link is Adani Ports and Special Economic Zone’s 70% stake in the Haifa Port in Israel. Port infrastructure is critical to pharmaceutical logistics. The Haifa connection creates a secondary channel through which conflict-induced port disruptions affect Indian corporate interests — and potentially pharmaceutical export routing to the region.

4. Supply Chain and Logistics Disruptions

4.1 The Strait of Hormuz: India’s Pharmaceutical Achilles’ Heel

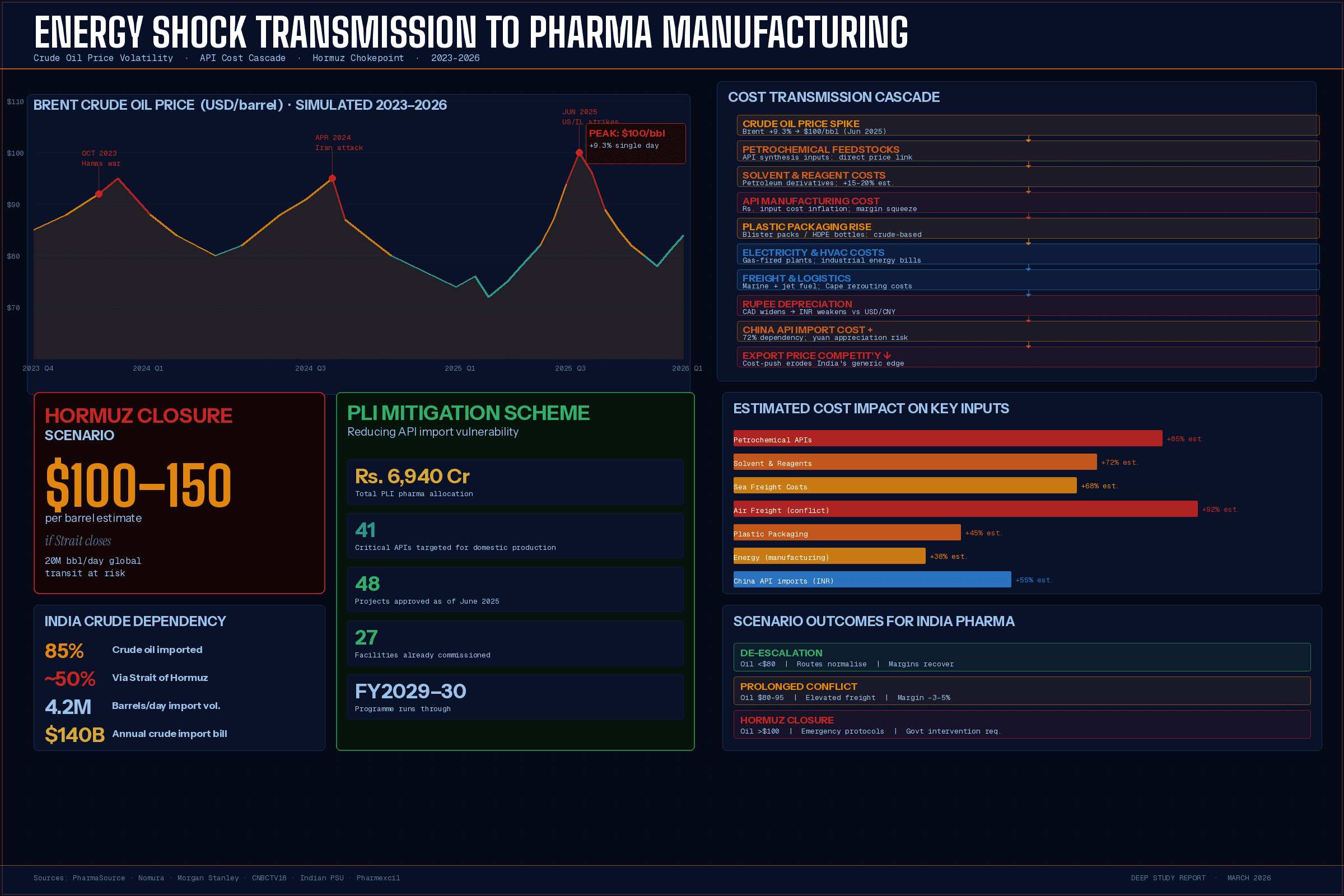

The most systemic threat posed by the Iran–USA–Israel crisis to Indian pharma is not direct pharmaceutical trade disruption but the potential closure or disruption of the Strait of Hormuz. This 21-mile-wide strait is the world’s most critical energy chokepoint, through which approximately 20 million barrels of oil per day — roughly 20% of global petroleum — transit daily.

| 20% Global Oil via Hormuz ~20M barrels/day | ~50% India Crude via Hormuz Per Nomura data (2026) | $100-150 Oil Price if Hormuz Closes Per barrel (est.) | 85% India Crude Import Dependence Imported |

India imports nearly 85% of its crude oil — approximately 4.2 million barrels per day. Nearly half of this transits through the Strait of Hormuz. For the pharmaceutical industry, the connection is through energy costs: higher crude prices directly increase electricity and HVAC costs at manufacturing facilities, raise petrochemical feedstock prices (critical for API synthesis), increase packaging material costs (plastics), and inflate freight and logistics costs across all supply chains.

| Industry analysis from PharmaSource estimates that a Hormuz closure could push oil prices to $100–150 per barrel, creating cascading cost increases across pharmaceutical manufacturing operations globally. India, as the ‘world’s pharmacy’, would face amplified production cost pressures that could compromise its competitive pricing advantage. |

4.2 Red Sea and Bab-el-Mandeb Disruptions

Since the Gaza war began in October 2023, Houthi attacks in Yemen (an Iran-aligned group) have forced most major container shipping companies to reroute vessels away from the Red Sea and Suez Canal to the longer Cape of Good Hope route. This has significantly extended transit times for Indian pharmaceutical exports bound for European markets and increased freight costs substantially.

The continued Red Sea tensions — a direct consequence of the broader Iran-Israel conflict ecosystem — have added persistent logistical pressure and elevated shipping insurance premiums for Indian pharmaceutical exporters.

4.3 Airspace Closures: Immediate Crisis Impact

The March 2026 escalation produced the most immediate and visible logistics disruption through widespread Middle East airspace closures. Westbound flights from India — including to the UAE, Saudi Arabia, Israel, Qatar, and destinations in Europe — were cancelled or rerouted as conflict zones expanded.

Air India cancelled all flights to and from the UAE, Saudi Arabia, Israel, and Qatar, with some New Delhi–Europe routes also affected. Alternative routes added up to 4 hours of additional flight time, dramatically increasing air freight costs for time-sensitive pharmaceutical shipments. Aviation expert Mark D. Martin estimated the weekly impact to Indian and international airlines at a conservative Rs 875 crore (approximately $96 million).

4.4 Shipping Cost Escalation for WANA Region

India exports pharmaceutical products worth $1.75 billion to the West Asia and North Africa (WANA) region — approximately 5.7% of total pharmaceutical exports in FY25. Key destinations include Iraq ($228.41M), UAE ($378.54M), Egypt ($212.84M), and Saudi Arabia ($211.73M). These exports primarily consist of finished dosage forms such as tablets, capsules, and syrups, along with generic drugs and biosimilars.

Industry executives noted that while no immediate demand shock has materialised as of early 2026, the disruption to sea and air routes is adding cost pressure to supply chains. Questions remain about how incremental logistics costs will be absorbed — through the value chain, through price increases, or through margin compression.

5. Energy Costs and API Manufacturing Economics

5.1 Crude Oil Price Volatility and Pharma Input Costs

Pharmaceutical manufacturing in India is energy-intensive. Active Pharmaceutical Ingredient (API) synthesis involves complex chemical reactions requiring consistent, high-volume energy supply. Solvent recovery, distillation, fermentation, and downstream processing all depend on reliable, affordable energy. When crude oil prices spike due to Middle East tensions, this creates multi-layered cost pressures.

Following US and Israeli strikes on Iran in June 2025 — which killed Iranian Supreme Leader Ayatollah Ali Khamenei — Brent crude prices hit a 52-week high, surging 9.3% to $79.40 a barrel in a single day. Morgan Stanley noted in a contemporaneous analysis that every $10 per barrel sustained rise in oil prices hits Asia’s GDP growth by 20–30 basis points.

| Cost Element | Linkage to Crude Oil | Impact Level |

| Petrochemical feedstocks | Direct API synthesis inputs; price-linked to crude | High |

| Solvents and reagents | Used in chemical synthesis; petroleum derivatives | High |

| Packaging materials (plastics) | Blister packs, HDPE bottles; crude-based | Medium |

| Electricity generation | Powers manufacturing facilities; gas/fuel dependent | Medium |

| Freight and logistics | Sea and air transport; jet fuel & marine fuel | High |

| API from China | 72% of India’s bulk drug imports; logistics costs rise | High |

5.2 China API Dependency: A Compounding Vulnerability

India’s pharmaceutical manufacturing faces a structural vulnerability that the geopolitical crisis has exposed more starkly. Approximately 72% of India’s overall bulk drug and intermediate imports in FY24 came from China (up from 66% in FY22). When both the Iran–Israel conflict disrupts energy markets AND US–China trade tensions raise tariff risks, India’s API supply chain faces simultaneous pressures from multiple directions.

The government’s Production Linked Incentive (PLI) scheme has approved 48 projects to domestically produce 41 critical pharmaceutical ingredients, with 27 already commissioned as of June 2025. This policy response directly addresses the conflict-exposed vulnerability but will take years to fully materialise.

5.3 Rupee Depreciation and Import Cost Escalation

Higher crude prices mechanically weaken the Indian rupee through widening of the current account deficit. A weaker rupee increases the landed cost of API imports from China (denominated in yuan/USD), raises the cost of imported laboratory equipment and instrumentation, and inflates repayment obligations for foreign currency-denominated debt. This currency transmission mechanism amplifies the pharmaceutical sector’s exposure to oil price shocks arising from Middle East tensions.

6. Impact on Key Indian Pharmaceutical Companies

6.1 Companies Most Exposed to Conflict

Industry experts and equity analysts have identified a spectrum of exposure among listed Indian pharmaceutical companies, ranging from direct operational impact to indirect demand and cost risks:

| Company | Exposure Level | Key Risk Factor |

| Sun Pharma | Very High | Majority stake in Taro Pharma, Haifa, Israel; direct conflict-zone exposure |

| Dr. Reddy’s | High | Significant MENA region presence; API supply chain complexity |

| Lupin | High | MENA market presence; logistics cost sensitivity |

| Torrent Pharma | Medium-High | MENA distribution networks; shipping cost exposure |

| Divi’s Labs | Medium-High | API manufacturer with export-heavy model; freight costs |

| Cipla | Medium | GCC market demand exposure; indirect energy cost impact |

| Biocon | Medium | Biosimilar exports; demand-driven risk from GCC slowdown |

| Punjab Chemicals | Medium | 5% revenue from Israel (FY24); direct market exposure |

6.2 Demand-Side Risks for GCC-Present Companies

For companies like Cipla and Biocon, the risk is less about operational disruption and more about demand dynamics. A slowdown in Gulf Cooperation Council (GCC) economic activity — caused by conflict-related uncertainty, oil revenue volatility, or consumer confidence erosion — can impact distributor payments, elongate receivable cycles, and soften regional healthcare spending.

Currency volatility in the GCC, particularly for non-pegged currencies, can also affect the economics of pharmaceutical imports. While such developments rarely cause immediate revenue contraction, they influence quarterly guidance and working capital efficiency.

6.3 Stock Market Reactions

Indian equity markets have responded to each escalation in the Iran–Israel crisis with pharmaceutical sector volatility. The BSE Healthcare Index declined approximately 2% in the week ended October 4, 2024, reflecting investor concern about Middle East exposure. Individual stocks like Sun Pharma saw targeted selling pressure due to Taro’s direct exposure. Market analysts flagged the ‘sell-on-recovery’ strategy adopted by institutional investors during periods of escalation.

7. India’s Strategic Balancing Act

7.1 Diplomatic Tightrope Between Iran and Israel

India’s predicament is uniquely complex: it maintains strategic relationships with both Iran and Israel, has direct economic interests in both countries, and faces US pressure to align with Western positions. This has compelled India to adopt a carefully calibrated diplomatic stance.

India distanced itself from the Shanghai Cooperation Organisation’s official stand on the conflict and urged both Israel and Iran to use existing channels of dialogue and diplomacy. India’s Ministry of External Affairs issued a statement calling for ‘immediate de-escalation, exercise of restraint, stepping back from violence and return to the path of diplomacy.’

7.2 The Chabahar Port Dilemma

Iran’s Chabahar Port is of critical strategic importance to India, providing access to Afghanistan, Central Asia, and beyond while bypassing Pakistan. Indian Ports Global Limited executed a 10-year operational contract with Iran’s Maritime Organisation for Chabahar. Any escalation that results in additional US sanctions on Iran — or direct conflict damage to Iranian infrastructure — threatens this strategic connectivity investment and the trade corridors it enables, including pharmaceutical logistics.

7.3 US Tariff Threats on Iran Trade Partners

In January 2026, the Trump administration threatened to impose an additional 25% tariff on countries trading with Iran — a direct threat to India’s pharmaceutical export surge to Iran. This created an acute policy dilemma: Indian pharma had just achieved a five-year record in Iran exports (up 70% in 2025), but this success could trigger US secondary sanctions pressure.

| India’s situation encapsulates the broader challenge facing emerging market economies in an era of weaponised trade and sanctions: the need to balance economic opportunity, strategic relationships, and great-power compliance demands — all simultaneously. |

8. Geopolitical Opportunities for Indian Pharma

8.1 Consolidating MENA Market Position

Crisis conditions, counterintuitively, can create pharmaceutical market opportunities. As regional conflicts disrupt supply chains from European and US pharmaceutical companies, Indian generics — already present in MENA healthcare systems — benefit from emergency procurement and substitution purchasing. The proven quality of Indian generic manufacturers, combined with cost competitiveness, positions Indian companies to consolidate market share during disruption periods.

8.2 The China+1 Strategy in Pharma

The conflict and associated sanctions have highlighted the geopolitical risks of supply chain concentration. Western pharmaceutical companies accelerating ‘China+1’ diversification strategies increasingly look to India as the preferred alternative manufacturing base. India’s PLI scheme for pharmaceuticals has already yielded 35 new API facilities, making it a credible recipient of this diversification investment.

8.3 Medical Tourism Dislocation

India’s medical tourism sector, which received approximately 644,387 foreign tourist arrivals in 2024 with West Asia accounting for nearly 18% (around 115,000 patients), faces near-term disruption from conflict-related travel uncertainty. However, as Iran’s domestic healthcare system is strained by sanctions and military conflict, and as patients from GCC nations face disrupted options, India’s world-class hospitals and affordable treatment costs position it to absorb redirected medical tourism from the region once stability returns.

8.4 Free Trade Agreement Tailwinds

India’s newly signed comprehensive trade agreements provide structural support for pharmaceutical exports even in a turbulent geopolitical environment. The India–UK Comprehensive Economic and Trade Agreement (signed July 2025) and the India–EFTA Trade and Economic Partnership Agreement (in force October 2025) both provide zero-tariff access for several pharmaceutical products in key regulated markets, improving the economics of export-oriented manufacturing.

9. Risk Mitigation Strategies

9.1 Industry-Level Responses

Indian pharmaceutical companies and industry associations have begun implementing multi-layered risk mitigation in response to the geopolitical environment:

- Strategic inventory buffering: Shifting from just-in-time to 60+ day buffer stock policies for critical APIs and raw materials exposed to Middle East supply routes.

- Logistics route diversification: Pre-qualifying alternative sea routes (Cape of Good Hope), alternate air freight corridors, and multi-modal combinations to reduce Hormuz and Red Sea dependency.

- Supplier contingency development: Pre-qualifying alternate API and feedstock vendors outside Gulf-dependent corridors to reduce single-point-of-failure risks.

- Contractual cost-sharing provisions: Negotiating force majeure and cost-escalation clauses in long-term supply contracts to distribute geopolitical risk across the value chain.

- Currency hedging: More sophisticated use of forward contracts and natural hedging to manage rupee volatility driven by oil price shocks.

9.2 Government Policy Responses

India’s government has responded to geopolitical supply chain risks with several targeted policy instruments:

- PLI Scheme for Critical APIs: Rs. 6,940 crore (approximately $834 million) allocated to support domestic manufacturing of 41 critical pharmaceutical ingredients through FY2029–30. As of June 2025, 48 projects approved, 27 commissioned.

- Bulk Drug Parks: Development of dedicated pharmaceutical manufacturing zones to create clustering advantages and reduce logistics costs within India.

- Pharmexcil Engagement: Active diplomatic outreach by the Pharmaceutical Export Promotion Council to maintain and expand market access in conflict-affected regions.

- Trade Agreement Diversification: New FTAs with UK and EFTA reduce dependence on conflict-sensitive markets.

9.3 Company-Level Best Practices

| Strategy | Implementation Action |

| Tactical supply audit | Flag all SKUs with Gulf-sourced materials or Hormuz-dependent logistics |

| Inventory strategy shift | Move from transactional to strategic buffer holdings (60+ day targets) |

| Logistics re-routing | Negotiate contracts through safe corridors, accounting for insurance costs |

| Intelligence monitoring | Establish energy and shipping intelligence networks for early warning |

| Regulatory engagement | Proactively discuss potential pricing and supply volatility with regulators |

| Supplier pre-qualification | Prequalify alternate API vendors outside the Gulf corridor |

| Financial hedging | Implement systematic currency and commodity hedging programmes |

10. Outlook and Projections

10.1 Short-Term Outlook (2026)

The immediate outlook is characterised by elevated uncertainty. The March 2026 escalation has produced immediate airspace closures, shipping disruptions, and oil price spikes. Indian pharmaceutical companies with MENA exposure are reviewing shipment schedules and logistics contracts. The rupee faces depreciation pressure from a widening current account deficit.

However, the structural resilience of Indian pharmaceutical exports — demonstrated by 9.4% growth in FY25 despite geopolitical headwinds — suggests the sector will absorb near-term disruptions without catastrophic impact, provided hostilities do not result in a sustained Hormuz closure.

10.2 Medium-Term Scenarios (2026–2028)

Three scenarios frame the medium-term outlook:

- Scenario 1 — Managed De-escalation: A ceasefire holds, shipping lanes normalise, and oil prices moderate. Indian pharma capitalises on its resilience narrative, consolidates MENA market share, and benefits from FTA-driven export growth. Iran trade gradually recovers under humanitarian exemption frameworks.

- Scenario 2 — Prolonged Low-Intensity Conflict: Continued Houthi attacks, periodic airspace closures, and elevated insurance premiums create a ‘new normal’ of elevated logistics costs. Indian companies adapt through re-routing and inventory strategies but face margin compression in MENA markets.

- Scenario 3 — Major Escalation / Hormuz Closure: A direct blockade or mining of the Strait of Hormuz triggers a global oil price shock ($100–150/barrel). India faces acute energy insecurity, rupee collapse, and API cost inflation. Pharmaceutical manufacturing costs rise sharply; export competitiveness erodes. Government emergency intervention required.

10.3 Long-Term Structural Shifts (2028–2030)

Regardless of the near-term conflict trajectory, the geopolitical crisis is accelerating structural shifts that will reshape Indian pharma’s global position:

- Domestic API self-sufficiency will improve through PLI-driven investment, reducing Iran-route vulnerability and Chinese dependency.

- Indian companies will increasingly build manufacturing presence within the MENA region itself, reducing cross-border logistics exposure.

- The Iran market will remain a latent opportunity — a population of 92 million with sophisticated pharmaceutical needs — that Indian companies will re-enter when sanctions frameworks evolve.

- India’s diplomatic capital with both Israel and Iran positions it uniquely as a potential pharmaceutical intermediary as both countries seek to rebuild health system resilience post-conflict.

11. Conclusions

The Iran–USA–Israel crisis has had multidimensional impacts on India’s pharmaceutical industry — simultaneously threatening existing trade relationships, disrupting logistics infrastructure, inflating energy and input costs, creating corporate-level operational risks, and reordering competitive dynamics in key export markets.

The most severe impact has been the near-destruction of India–Iran pharmaceutical trade, driven not by direct pharmaceutical sanctions but by the collapse of payment mechanisms following US oil sanctions. A relationship worth $205 million in FY20 has shrunk to $40.66 million in FY25 — a loss that has materially benefited Chinese competitors.

The Sun Pharma–Taro nexus represents India’s most direct corporate-level vulnerability, with a major pharmaceutical asset directly located in an active conflict zone. The broader energy price transmission mechanism — through the Strait of Hormuz — poses systemic, economy-wide risks that dwarf direct pharmaceutical trade impacts.

Yet the crisis has also revealed India’s pharmaceutical sector’s remarkable resilience. Despite escalating tensions, FY25 exports surged past $30 billion. New FTAs, PLI investments, and improving domestic API capabilities are building structural buffers against geopolitical shocks. India’s unique diplomatic positioning — maintaining credible relationships with both Iran and Israel — could ultimately translate into pharmaceutical market advantages as the region rebuilds.

| Strategic Conclusion: India’s pharmaceutical industry is structurally resilient but geopolitically exposed. The sector’s future competitiveness depends on reducing API import concentration, diversifying logistics routes, deepening MENA market relationships, and leveraging India’s diplomatic capital to maintain access to contested markets. |

References

The following sources were consulted in preparing this report:

- Business Standard (March 3, 2026). ‘Drugmakers may review shipment schedules to West Asia if conflict drags on.’ business-standard.com

- CNBC (March 2, 2026). ‘India hit by high oil prices, flight cancellations amid Iran conflict.’ cnbc.com

- BusinessToday (January 13, 2026). ‘Trump Iran Tariffs: India’s pharmaceutical exports to West Asian country hit record high in 2025.’ businesstoday.in

- Organiser (December 19, 2025). ‘Indian pharma exports surge past USD 30 billion, mark 9.4% growth in FY 2024-25.’ organiser.org

- The Financial World (June 20, 2025). ‘Talent and Trade: Indian Pharma Industry bonds with Israel and Iran.’ thefinancialworld.com

- PharmaSource (June 23, 2025). ‘Iran and Strait of Hormuz Crisis – Impact on Pharmaceutical Supply Chain.’ pharmasource.global

- PharmaSource (July 25, 2025). ‘How Geopolitical Tensions Disrupted Pharma Supply Chains in Q3 2025.’ pharmasource.global

- Supply Chain Wizard (August 2, 2025). ‘Rebalancing Pharma Supply Strategy Amid 2025’s Geopolitical Shifts.’ supplychainwizard.com

- ISPE Pharmaceutical Engineering (March–April 2025). ‘Indian Pharmaceutical Industry: Creating Global Impact.’ ispe.org

- Bain & Company (2025). ‘Healing the World: A Roadmap for Making India a Global Pharma Exports Hub.’ bain.com

- IBEF (2025). ‘Pharmaceutical Industry — Pharmaceutical Exports from India.’ ibef.org

- Jago Grahak Jago / Pharmabiz (April 2024). ‘Middle East crisis escalation may hurt pharma exports.’ jagograhakjago.com

- BusinessToday (October 5, 2024). ‘Iran-Israel Conflict: These listed companies on D Street may feel jittery.’ businesstoday.in

- BusinessToday (October 11, 2023). ‘How Israel-Hamas war will impact Indian pharma exports.’ businesstoday.in

- PharmaSource (December 4, 2023). ‘Impact of Israel-Hamas War on the Pharma Supply Chain.’ pharmasource.global

- Business Standard (October 1, 2023). ‘Indian pharma exports to Iran decline thanks to its lower rupee reserves.’ business-standard.com

- Iran International (October 26, 2025). ‘Iran faces looming medicine shortages as UN sanctions strain drug supply chains.’ iranintl.com

- Indian PSU (March 2026). ‘Iran–Israel Conflict: What Rising Geopolitical Tensions Mean for Petroleum Prices in India.’ indianpsu.com

- Pharmexcil (2025). Hand Book 2025. pharmexcil.com

- All Indians Matter. ‘How a widening Middle East conflict would affect India.’ allindiansmatter.in

- Sahi.com. ‘Iran Israel Conflict Impact on Indian Stocks: Oil, EPC & Aviation Risk.’ sahi.com

- IQVIA (2024). ‘White Paper: Localization of Pharmaceutical Manufacturing in Middle East and North Africa Region.’ iqvia.com

- Ministry of External Affairs, Government of India. Country Brief: Iran. mea.gov.in

- NITI Aayog Trade Watch (Q1 FY26). India Trade Analysis. niti.gov.in